A head-to-head matchup of electric and gasoline cargo trucks shows how rising fuel costs make EVs much cheaper to run. Now, can manufacturers lower up-front costs?

Electric cargo trucks have been getting more cost-competitive for years. But the fuel price spike triggered by the Iran war has made it clear just how much cheaper it can be to move freight with trucks that run on electricity instead of gasoline or diesel.

New data from electric-vehicle manufacturer Workhorse, which runs identical routes with both gasoline cargo trucks and electric cargo trucks for its Stables by Workhorse business, provides a case study of how elevated gasoline prices make EV options more appealing.

Stables delivers packages as an independent service provider for FedEx in Ohio. Its use of internal-combustion-engine and battery-electric trucks side by side has given it a rare “controlled, real-world comparison” of the two vehicle classes with “the same routes, the same drivers, and the same weather,” as explained in a presentation at the ACT Expo trucking industry show in May.

The electric trucks Workhorse builds and runs in its Stables fleet, a type known as step vans, were already cheaper to operate last year than their gasoline-fueled counterparts — saving about 42.5 cents per mile, based on electricity at 11 cents per kilowatt-hour and gasoline at $2.98 per gallon.

But by May 1, gasoline had spiked to an average of $4.83 per gallon in Ohio, pushing the savings advantage for electric trucks up to 73.6 cents per mile. With gas prices so high, a Workhorse step van driving about 50 miles per day can expect to save about $11,000 per year on fuel costs.

The operating-cost difference matters a lot when it comes to electrifying truck fleets. EV trucks cost 50% to 100% more than fossil-fueled versions, according to industry estimates, which means they need to provide enough savings on operations to make up for that higher sticker price.

In the past few months, Workhorse CEO Scott Griffith said customers have grown more interested in buying trucks from his company, which is a small-scale producer in the broader world of medium-duty truck manufacturing.

“The phone is certainly ringing, and the interest is high, and everyone’s doing the math,” he said. “What is the cost of electricity, what are the lease costs, what are the operations and maintenance costs? They’re coming in with a much more sophisticated approach.”

Workhorse’s experience is only one example of how EV trucks are growing more appealing to fleet operators, said Corey Cantor, research director at the Zero Emission Transportation Association trade group. He noted that other fleet operations have observed similarly high savings as gas and diesel prices have spiked in recent months. While those prices have declined slightly since a purported peace deal between the U.S. and Iran last month, they remain significantly higher than before the war began.

Diesel, which is the primary fuel for trucks around the world, has seen an even greater increase in cost than gasoline, putting pressure on fleet operators.

“When diesel is at such an elevated price — even if it may come down over the longer term — it spurs a conversation,” Cantor said.

While the recent gasoline and diesel price spikes are driving conversations about electrification, it’s not clear whether that’s resulting in more purchases or leases of EV trucks.

That’s mainly because the data hasn’t yet come in, said Jacob Richard, technical project manager at Calstart, a nonprofit group whose members include energy producers, carmakers, and other businesses.

There’s plenty of room for growth. Electric trucks made up less than half a percent of the total U.S. truck stock as of mid-2025, according to Calstart’s January report Zeroing in on Zero-Emission Trucks.

Of the 72,000 electric trucks deployed in the U.S. at the end of last year, the vast majority were so-called “last-mile” delivery vans. Cargo vans — the smallest type of commercial cargo vehicle — are an ideal electrification target because they run relatively short routes to and from central depots where they can recharge overnight using slower, less-expensive charging infrastructure, said Mike Roeth, executive director of the North American Council for Freight Efficiency.

The nonprofit research group has put vehicles through real-world tests in its “Run on Less” events and found that battery-electric trucks cost less to operate than fossil-fueled equivalents on the sub-100-mile daily routes that make up about half of all freight miles traveled in the U.S.

Griffith agreed that shorter-haul, “return-to-base” freight routes have been a good fit for Workhorse customers like Purolator and Gateway Fleets, both of which have placed orders for 100 of the company’s electric step vans this year.

“Many of them are running what we call lollipop routes — 90 miles out from the depot, and coming back and charging up,” Griffith said. He added that “a significant chunk of medium-duty trucks” are running such routes, “especially the large fleets.”

But electrifying medium-duty trucks is more complicated than electrifying cargo van fleets, Roeth noted. Medium-duty trucks range from step vans like the ubiquitous brown UPS delivery vehicles to box trucks that have different types of rectangular cargo containers mounted on separately built “cutaway” chassis. They tend to be built for a wider variety of custom markets in much lower quantities than cargo vans, which more closely resemble mass-market passenger vehicles in how they’re manufactured and marketed.

“The smaller and more automotive you are, the greater the scale of production, the lower the cost,” Roeth said. “As you move to a cutaway, where you have to work with a different manufacturer to get that box on, the cost challenges go up.” That’s true for both EV and internal-combustion vehicles in this class, he said.

Still, manufacturers of battery-electric trucks stand a good chance of making headway across market segments while fuel prices are high, Cantor said.

He highlighted Harbinger Motors, a startup that manufactures medium-duty electric-vehicle chassis that can be customized for different classes of vehicles. The California-based startup has raised about $360 million in venture financing, including a $160 million round in November co-led by FedEx, which also ordered 53 of the company’s medium-duty truck chassis.

Workhorse has taken a more circuitous route, Roeth said. He worked at the company back when it was an affiliate of Navistar International making chassis for internal-combustion-engine trucks. In 2013, Workhorse was acquired by startup AMP Electric Vehicles and shifted to making battery-electric chassis.

Last year, it merged with long-time electric-chassis startup Motiv, in what Roeth described as “a perfect marriage.” Even so, it’s not easy to break into established medium-duty truck markets: Workhorse reported widening losses in its first earnings report as a combined company in the first quarter of this year, despite increasing revenues.

Those losses were driven in part by higher investments in manufacturing, as Workhorse retools its factory in Union City, Indiana, for the latest generation of its all-electric chassis, featuring more efficient batteries, drivetrains, and power-control systems. That factory is capable of producing up to 5,000 vehicles per year.

“We’re not just sticking an electrified powertrain on what we currently sell,” said Griffith, who was CEO at Motiv before the merger. “You can get some efficiencies out of that. But you can’t capture the full benefits of a fully software-defined vehicle without going all the way.”

The primary barrier to fleet electrification is the up-front cost of electric trucks. Right now, “a standard rule of thumb is that these vehicles are going to cost two times more than the equivalent cost of a diesel or gasoline version,” Calstart’s Richard said.

But there’s a lot of variation. Commercial vehicle pricing data “is not as transparent and easy to access as [data on] passenger cars,” Cantor said. Many vehicles are custom-designed, and pricing varies greatly depending on factors such as bulk purchase orders and preexisting relationships with fleet operators.

In the case of Workhorse, Griffith estimated that the company’s electric step vans cost about 30% to 40% more than comparable fossil-fueled vehicles. In early April, Workhorse dropped the price of its standard-sized W56 battery-electric step vans by roughly $60,000 to bring them just under $200,000 apiece, about level with the highest-end gasoline- or diesel-fueled alternatives.

The payback time on an electric truck depends on a mix of things — the model, state incentives, fuel prices, and so on. In states like California and Washington, which have generous incentives, buyers can recoup the extra costs on Workhorse’s larger step-van model in three to five years depending on gas prices, according to the company’s chief communications officer, John Williams.

Whether these kinds of paybacks are fast enough will depend on the fleet operator.

In general, bigger operators can afford to take a risk and wait longer, according to Richard. But Calstart presumes that the majority of buyers need to see a payback in three years, which coincides with how they structure financing and resale planning for their internal-combustion fleet vehicles, he said.

Today, the vast majority of electric trucks are being bought by big corporations that have both the deep pockets and the sustainability goals to make the up-front costs worth absorbing, Griffith said.

“But this is a $23 billion-a-year industry,” he said, citing estimates of annual U.S. sales of medium-duty vehicles — and to meet the needs of the broader market, “we’ve got to get the price point down.”

In certain regions, government incentives can nearly close that price gap, Richard said. Though the Trump administration and Republicans in Congress erased many of the federal tax credits that incentivized EV purchases, some EV-friendly states still provide incentives and rebates, he noted. “It makes sense for fleets to capture those up-front incentives while they stand.”

But electric truck manufacturers can’t bank on government incentives, Griffith said. “Those dollars are disappearing in the coming years. The industry has to get to the point where [total cost of ownership] blows internal combustion out of the water — and the buying price of an EV has to be closer to a 10% premium.”

To be clear, electric trucks offer significant benefits beyond lower fueling costs, Roeth said. Companies participating in his organization’s Run on Less events have tracked financial benefits like significantly lower maintenance costs as well as perks like increased driver comfort. Plus electric trucks release much less carbon and local air pollution — an important improvement, as commercial trucks are responsible for a disproportionate amount of such emissions from the U.S. transportation sector.

“For good or for bad, these trucks are used in routes that are sitting and idling for long periods of time,” Griffith said. “They emit three or four times per mile the emissions and carbon you get out of a passenger car. And they’re on routes that tend to affect dense populations,” he said.

Ultimately, he said, “if we can improve the economics and emissions together, make everything better on that route, fleets are going to adopt it.”

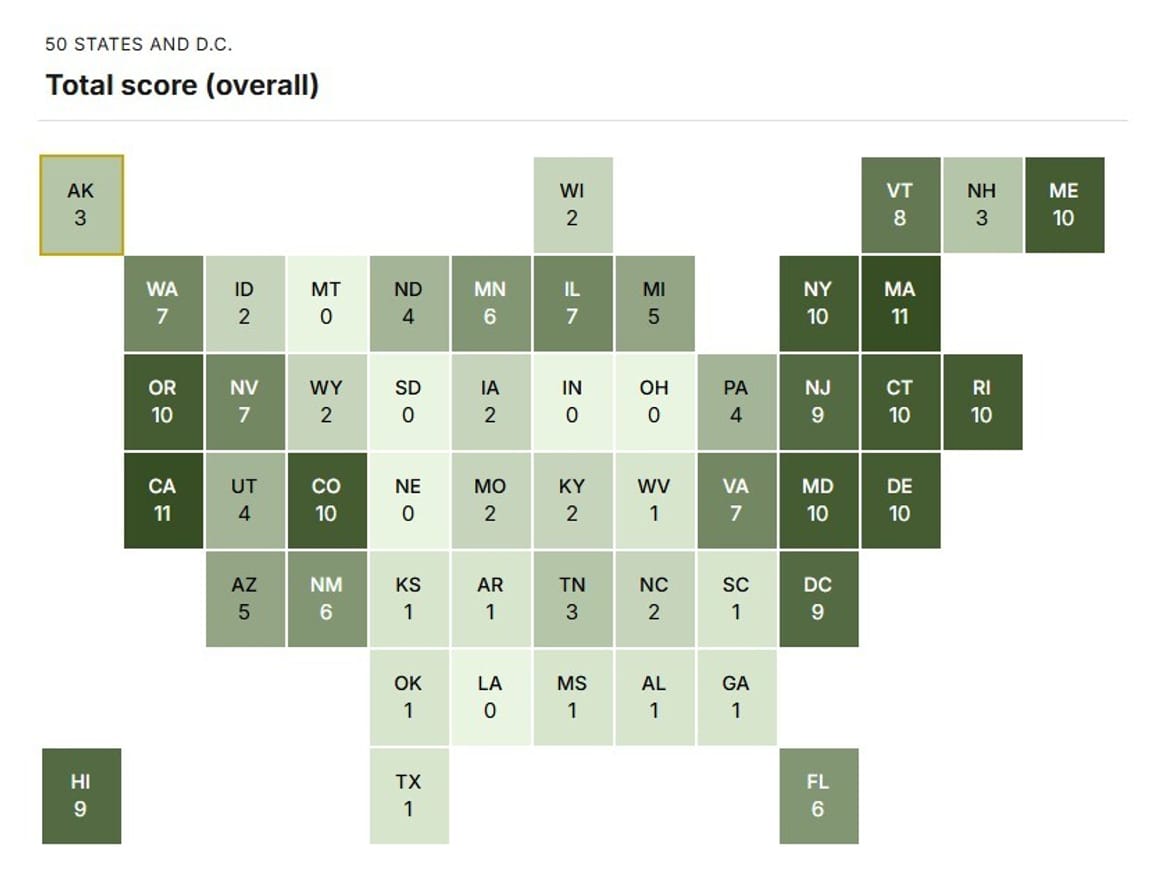

California, Massachusetts, and several other states are home to robust charging networks and strong consumer incentives that make it easy to go electric.

America’s EV industry has suffered a series of bad breaks over the last year and a half.

The end of federal tax credits for electric vehicles sent sales of new EVs off a cliff last fall. A nationwide buildout of chargers has been slow to get rolling. And the Trump administration has been dismantling air pollution regulations that were nudging the country away from gas cars.

But in the absence of a federal push for EVs, several states have been picking up the slack by building strong charging networks, introducing consumer incentives, and adopting other policies that make going electric a sweeter prospect.

A new analysis from the Brookings Institution dives deep on what makes a state an EV oasis, and scores states based on how far they’ve gone to promote vehicle electrification. At the top of its ranking? It’s a tie between California and Massachusetts, both of which scored 11 out of 13 possible points for overall EV readiness.

Massachusetts, New York, and Connecticut, meanwhile, have three major incentives to encourage average drivers to buy EVs: purchase rebates or tax credits, benefits like toll credits or parking perks, and no annual EV registration fees.

What about charging? Massachusetts and New York are the winners here, as they both have robust public charging networks, rebates that help people install chargers, and special utility rates for charging.

And yet Massachusetts still has room for improvement, according to Brookings. For one, EV manufacturers aren’t allowed to service vehicles in the state, which also lacks a plan for building out EV-charging infrastructure. As for California, the state’s annual registration fee for EV owners and lack of special utility rates for charging are weak spots.

At the other end of the spectrum, six states — Indiana, Louisiana, Montana, Ohio, Nebraska, and South Dakota — don’t have a single policy in place that’s getting them ready for an EV future, according to Brookings. Nineteen more have just a few EV-boosting policies on the books. Clearly state action alone won’t be enough to propel the entire U.S. toward a cleaner driving future.

Coal plants forced to stay open aren’t producing much power

The Trump administration has effectively stopped fossil fuel power plants from retiring on its watch, despite the strategy providing little benefit to the power grid and racking up hefty costs.

Six power plants, five burning coal and one burning oil and gas, had been slated to retire by the end of 2025, but were instead ordered to stay running to prevent what the administration called an “energy emergency.” At least one of those coal plants hasn’t operated at all under the emergency order, and another ran for only about two weeks, according to federal data reviewed by Utility Dive.

Altogether, the five coal plants produced just 1.5 million megawatt-hours of power during the first quarter of 2026, down 65% from what they generated during the same period last year. At the same time, the plants have racked up hundreds of millions of dollars in costs that could end up coming out of utility customers’ pockets.

Hyundai is building a massive steel mill in Louisiana. Will its neighbors benefit?

Hyundai’s plans to build a steel and iron plant in Louisiana could drive a clean revolution — or add yet another polluting factory to an area already known as “Cancer Alley.”

Canary Media’s Maria Gallucci recently visited the rural stretch between New Orleans and Baton Rouge where Hyundai is building a massive facility that will produce steel for automaking. At first, the plant will use natural gas to melt iron into steel — already a lower-carbon alternative than the coal that powers aging steel mills in the Midwest. But Hyundai has said it may later power its furnaces with hydrogen made from renewable electricity.

In the nearby city of Donaldsonville, residents and local leaders told Maria they’re skeptical Hyundai will actually follow through. They’re already surrounded by petrochemical facilities and oil refineries, and worry this latest factory won’t be any better for residents’ health or job prospects.

Read Maria’s thorough take on a complex story to learn more about the perils and promises of Hyundai’s green steel plans.

Nuclear ball out: The Trump administration announces $17.5 billion in loans to spur the development of 10 large nuclear reactors, with aims to begin construction by 2030 and get plants up and running in the next decade. (Associated Press)

Pumped-up home sales: A new report finds that installing an all-electric heat-pump heating and cooling system can increase a home’s resale value — as long as the appliance is mentioned in the real estate listing. (Canary Media)

Raising the roof: Warehouse roofs could be the perfect place to build solar arrays that can bring low-cost clean power to communities that can’t install their own panels, but states and utilities first need to do more to promote these community solar projects. (Canary Media)

Slated for takeoff: Jeff Bezos–backed EV startup Slate Auto says it has more than 180,000 reservations for its low-cost, bare-bones electric pickup, and customers now have a chance to preorder a vehicle with a $300 deposit. (Axios)

A data center surprise: The House Energy and Commerce Committee’s top Democrat, Rep. Frank Pallone, unexpectedly calls for a nationwide moratorium on data center development as Congress crafts legislation to protect household utility bills from spiking because of data centers’ massive power demands. (E&E News)

Can electric vehicles finally start working as backup batteries for homes and the grid? This 120-home pilot project in California is working out the kinks.

At first glance, Frances Bell’s home in Oakland, California, doesn’t look like a postcard from the EV-powered future. But if a new program takes off, it could be a harbinger of what’s possible for homes across the state and the country.

Sure, there’s a shiny new Kia EV9 in the driveway and a black charging cord that runs from the car to an EV charger on the side of her house. But that’s a pretty standard setup in California, the nation’s leader in electrical vehicle adoption.

What makes this EV and the charger special is that they don’t just draw power — they also send it back to both Bell’s home and the grid.

As the CEO of Bidirectional Energy, Bell is outfitting homes across California with the same Wallbox Quasar 2 bidirectional direct-current charger that’s mounted to her house. This year, Bidirectional Energy and Wallbox are installing the equipment at about 120 homes as part of a state-funded pilot program that offers participants rebates for two-way chargers. Bell’s household was among the earlist to enroll, primarily to test the technology firsthand.

Their goal: to establish rules of the road for city and county permitting inspectors and utility interconnection engineers to handle these installations, similar to the standards for regular one-way EV chargers and backup batteries.

“From my perspective, a DC bidirectional charger is essentially the same technology as a solar or battery inverter,” Bell said. And those technologies are straightforward for a household to install.

Bidirectional systems are not anywhere near as simple to adopt. Pilot projects have been going on for decades, and federal and state governments have been working with automakers, charging manufacturers, and utilities to standardize the underlying technologies. Nevertheless, no large-scale programs exist today to allow customers to send power from their EVs to the grid or their homes.

If companies like Bidirectional Energy and Wallbox can crack the code on broader adoption, it could unlock serious benefits to the grid and consumers. Vehicle-to-grid (V2G) applications can turn cars into cheap energy storage for the electricity system and vehicle-to-home applications (V2H) can turn their cars into batteries that can power their house, saving them money.

Bell is convinced that the larger scale of this California program will help push the technology out of pilot purgatory and into the mainstream.

“Previous bidirectional demonstrations were in the ones and twos,” Bell said. “When you get to 100 or more, you start to get to more standard processes. That’s how you start to scale.”

On a sunny May afternoon, Bell showed off her bidirectional charging system — and the benefits it provides.

The combination of Wallbox’s hardware and Bidirectional Energy’s software can actively draw power from the battery of a Kia EV9 to reduce a household’s costly utility bills, to send power to the grid to prevent rolling blackouts, or to power a home during an outage. The system isn’t available for use with other EVs yet, though the companies are in discussions with undisclosed automakers.

“If the grid goes down, this will just kick in. You don’t have to walk out here and switch it,” Bell said. Then she flipped a switch in the Wallbox power recovery unit, which connects the Quasar 2 to Bell’s electrical meter and the grid beyond, to mimic a power outage.

With a click, Bell’s home was being powered by the Kia EV9’s battery, which stores about 99 kilowatt-hours of energy. That’s as much as seven Tesla Powerwall batteries, and enough to keep a typical home powered for about three days, Bell said.

Next, Jessica Kwong, Bidirectional Energy’s senior software engineer, sent instructions from her laptop to the company’s software platform to curb grid power use to avoid high time-of-use rates. Bell opened the Bidirectional Energy app on her iPhone to track the shift in home power coming from the EV battery. Then she toggled to a screen that showed the money she’s saving on her utility bill.

“Every day, when I plug in my car, this number ticks up,” Bell said.

Finally, Kwong mimicked a demand-response event, when utility customers are asked to either send stored energy back to the grid or simply use less energy when the grid is under stress. The EV’s battery started delivering 12.5 kilowatts of steady power back to the grid — and earning money for the grid relief it was providing.

None of this is particularly groundbreaking from a technical perspective, said Bell, who’s worked at battery companies including Tesla and Fluence and as a grid planner for Northern California utility Pacific Gas & Electric. And after years of work from automakers, charger manufacturers, and software companies, a lot of progress has been made on setting the technology standards for bidirectional charging, she said.

That’s why this Bidirectional Energy and Wallbox project, funded by the California Energy Commission, is focused on more than simply proving the technology works, she said.

“We’re training some of the first installers, we’re getting the first interconnection processes established, and hoping to take that to other geographies.”

Bidirectional charging is an intuitive idea: Most cars spend most of their lives parked, which means that EVs are often sitting there with unused battery capacity that could be helping the grid, making money, or providing emergency backup services.

Lots of utilities are working on managed-charging programs, which ask customers to shift when their EVs pull power from the grid, whether to mitigate their contribution to peak power demand or to avoid overloading local circuits and transformers. That’s important, but it ignores EV batteries that could actively bolster the grid, not just reduce strain on it.

In California, the value of that latent EV capacity could be “an order of magnitude larger” than simply throttling EV charging, according to a 2021 study by University of California, Irvine, professor Brian Tarroja and Rochester Institute of Technology professor Eric Hittinger. It could also provide EV owners with thousands of dollars per year in utility bill savings and demand-response revenue, the report found.

Still, the approach has remained elusive — something of a holy grail for the EV industry.

Automakers have promoted these kinds of uses for years, from the earliest Nissan Leaf EVs to the now-discontinued Ford F-150 Lightning. Some automakers have designed their own vehicle-to-home connectors, as with the PowerShift charger from General Motors’ GM Energy business and Tesla’s Backup Switch for enabling Cybertruck Powershare mode. A growing number of EV-charger manufacturers make bidirectional-capable chargers that have been certified for use in California and in other states.

Many other states are pushing utilities to explore the concept, too, whether it’s using electric school buses as grid batteries or enabling homes to rely on plugged-in EVs for grid relief.

But California has set a goal of having 8 million light-duty EVs on its roads by 2030, making it ground zero for development via utility trials, state-funded pilot programs, and regulatory guidelines for streamlining bidirectional charger interconnections.

Wallbox, a Spanish company that does a lot of business in Europe, has seen a big uptick in North American sales in recent years, “especially when we talk about V2G,” said Oliver Waterhouse, the company’s director of strategic partnerships.

But injecting power from EV batteries to the grid “requires collaboration with utilities and grid operators,” he said — and while customers are eager to set up their EVs as backup batteries, “a lot of demand falls off when it takes 6 to 9 months to get an interconnection complete.”

Wallbox initially launched the Quasar 2 in partnership with Kia as a home backup system, he said. “Then Bidirectional Energy came in and said, ‘Let’s make it V2G as well.’”

One of the trickier tasks for the two companies has been getting the components of the bidirectional system to feel like a single streamlined experience for the customer, Bell said. To achieve this, the companies have been establishing the linkages between onboard EV-battery management systems, the controls embedded in the chargers, and the inverters within those chargers, which deliver power to the home and the grid, Bell said.

Industry groups and certification organizations have settled on a plethora of technology standards for handling those tasks. But every automaker and charger manufacturer may implement them slightly differently, which means each combination has to go through its own round of testing.

Automakers also need to make sure cars are charged when drivers need them to be. “First and foremost, you want your car to be a car,” Bell said. Bidirectional Energy’s software allows customers to set what time in the morning they want to be fully charged and establish limits on how much power can be pulled from their EV batteries, she said.

Getting utilities to trust that these underlying controls can safely send power back to the grid has been the next challenge, Waterhouse said. Wallbox has gone through these processes with all three of California’s major utilities, he said, “but when you submit interconnection applications, they all have different questions.”

This is where doing hundreds of installations, as is the plan for the second phase of the Wallbox and Bidirectional Energy pilot, can start to smooth things out, Bell said. Utilities have sent engineers to pore over every detail of the first installations done by Wallbox and Bidirectional Energy, she said. That’s pretty similar to how utilities used to treat conventional home batteries, she noted.

“For solar and batteries today, there’s no engineer that gets sent to the house,” Bell said. “Getting these first 120 right will be really key for the next hundred or thousand — or million.”

A correction was made on June 9, 2026. The story misstated that bidirectional charging systems can export EV battery power to the grid during an outage.

Despite the state’s political embrace of EVs, it has built zero chargers nearly four years after receiving federal funds from the Biden administration.

For all the concern about lost federal funding courtesy of the Republican trifecta in Washington, Massachusetts still has not deployed a single electric vehicle charger through a Biden-era program that President Donald Trump has left intact.

The Bay State is sitting on the roughly $64 million it was awarded through the National Electric Vehicle Infrastructure (NEVI) program, a $5 billion federal initiative authorized through the 2021 bipartisan infrastructure law meant to strategically dot the nation’s major highways with charging infrastructure that would make it easier for EV drivers to reliably travel greater distances.

Two years ago, Massachusetts selected three vendors to identify locations for NEVI charging stations and then build and maintain them. Only contracts with two of those companies, however — Applegreen and Global Partners — are signed, the state’s Department of Transportation confirmed to CommonWealth Beacon, leaving open questions about the viability of the third vendor, Weston & Sampson.

Now, nearly four years after receiving federal approvals, no EV chargers on Massachusetts’s major roadways through NEVI are up and running, MassDOT also confirmed.

It’s not clear what exactly is causing the holdup. CommonWealth Beacon filed a public records request to view the contracts with the two companies to ascertain whether there are deadlines associated with charger installations, but MassDOT did not provide those contracts in time for publication.

“The slowness of adoption here is mystifying,” said Jim Aloisi, a former state transportation secretary who now lectures at the Massachusetts Institute of Technology and serves on the board of the advocacy group TransitMatters. “If your approach to transportation sector decarbonization is largely about the transition to EVs, then you should be spending a fair amount of effort accelerating the process of getting people to adopt EVs, and one way to do that is obviously to roll out the NEVI initiative. That’s the disconnect.”

MassDOT didn’t respond to questions about why the pace of NEVI work has been so slow. The department’s “conservative” projections in 2022 found that NEVI funding would be sufficient for building 92 charging ports.

Some officials serving on the state’s Electric Vehicle Infrastructure Coordinating Council, which was established in 2022 to help create an equitable and reliable charging network, also appear to be in the dark. Eric Bourassa, who is a member of the group and serves as the director of transportation for the Metropolitan Area Planning Council, said that he’s “not privy to the details of what’s holding it up,” but that “everyone would agree that the pace of NEVI deployment in Massachusetts has been disappointing.”

So far, the two signed NEVI vendors have spent close to $4 million, according to Marshall Hook, a MassDOT spokesperson, all of which are for “development-focused” activities like engineering, permitting, and procurement.

There have been signs of progress. Applegreen has placed an order for EV charging equipment for locations in Greenfield and Newburyport and is targeting late July to begin construction, Hook said. Global Partners, meanwhile, has been approved to place orders on equipment and is finalizing plans to install chargers in Lancaster, Wrentham, and Raynham.

James Cater, senior director for sustainability strategy and innovation at Global Partners, said in a statement that the company is “happy” to be working on Massachusetts’s NEVI program and is beginning the procurement process for contractors for their initial charging sites “soon.”

Applegreen and Weston & Sampson did not respond to requests for comment.

Yet the slow adoption rate through NEVI continues to bewilder transit advocates given the state’s relatively small size and political embrace of EVs. Neighboring states like Rhode Island, New York, and Vermont boast a significant stock of NEVI chargers, in addition to more sprawling red states like Utah and Ohio.

“We should be capitalizing on every opportunity that we have available to us,” said Anna Vanderspek, electric vehicle program director at the Green Energy Consumers Alliance. “MassDOT should explain why it’s taken so long and what timetable we can expect now.”

The uptake on NEVI has been slow nationwide: Just 19 states have at least one operating EV charger funded through the program, according to the National Association of State Energy Officials. Adie Tomer, a senior fellow at Brookings Metro who specializes in infrastructure policy, said that poor capacity more broadly across states has stifled their ability to quickly implement the program as they wrangle procurement processes, permitting, and electrical grid transmission complications.

“There were plenty of ingredients here to have paralysis by analysis,” Tomer said. “Government officials are naturally going to be risk averse, especially with newer programs, and officials needed to learn on the fly. NEVI hits all those sweet spots, so it’s not terribly surprising that deployments are coming along slower than initially hoped.”

The data around Massachusetts’s EV push offers a mixed bag. On one hand, the state’s slow crawl on NEVI is contrasted by its relative success deploying EV chargers in general. State data show the Commonwealth ranking fourth in the country for charging ports per capita after a sharp increase in installments over the past few years.

Yet, Massachusetts still has about 2,000 charging ports less than what it estimates it needs, according to the most recent state climate report card.

The state also remains significantly behind its targets for registered electric cars and trucks as it races to cut its greenhouse gas emissions in half compared to 1990 levels by 2030. There are just 735 medium-and-heavy-duty EVs on the road, a sliver of the 3,200 called for by the end of 2025.

On light-duty EVs and plug-in hybrids, Massachusetts has about 166,000 such cars, short of the 200,000 needed by last year. Last year, the Healey administration also delayed an EV sales requirement.

Part of convincing consumers to purchase generally more expensive electric cars involves easing “range anxiety,” the worry of EV drivers about whether they’ll make it to their destination or the next charging station — one of the core functions of the NEVI program.

Notably, Massachusetts has also placed its NEVI bet on two companies that have been at intense odds with each other in the past year.

Applegreen and Global Partners — the two vendors with signed contracts with the state for NEVI work — have been at the center of a bitter dispute over the state’s efforts to redevelop 18 highway service plazas. MassDOT awarded Applegreen that major contract last year, but the company backed out after losing bidder Global Partners sued the state and fought to block the deal over allegations that the process was unfair.

MassDOT is now preparing to rebid the whole project, and the state inspector general ridiculed the agency for having “too many flaws” in its process that has attracted the ire of Beacon Hill.

The bad blood between Applegreen and Global Partners may not spill over into how fast the companies can deploy chargers on the state’s major highways since they will be responsible for separate individual sites, minimizing the necessity for direct collaboration.

But the situation speaks to the challenges of complicated procurements and the fragility of the private market to perform this sort of work, when a small pool of companies competes for similar supplies and subcontractors and could be vulnerable to price spikes.

“The word ‘irony’ is a good one,” Aloisi said. “It may be that there’s just not a lot of good competition in this area. What does that landscape look like, and who wants to play in that sandbox? And it may be that the unfortunate answer is not too many players, so you’re stuck with the same.”

This article first appeared on CommonWealth Beacon and is republished here under a Creative Commons Attribution-NoDerivatives 4.0 International License.

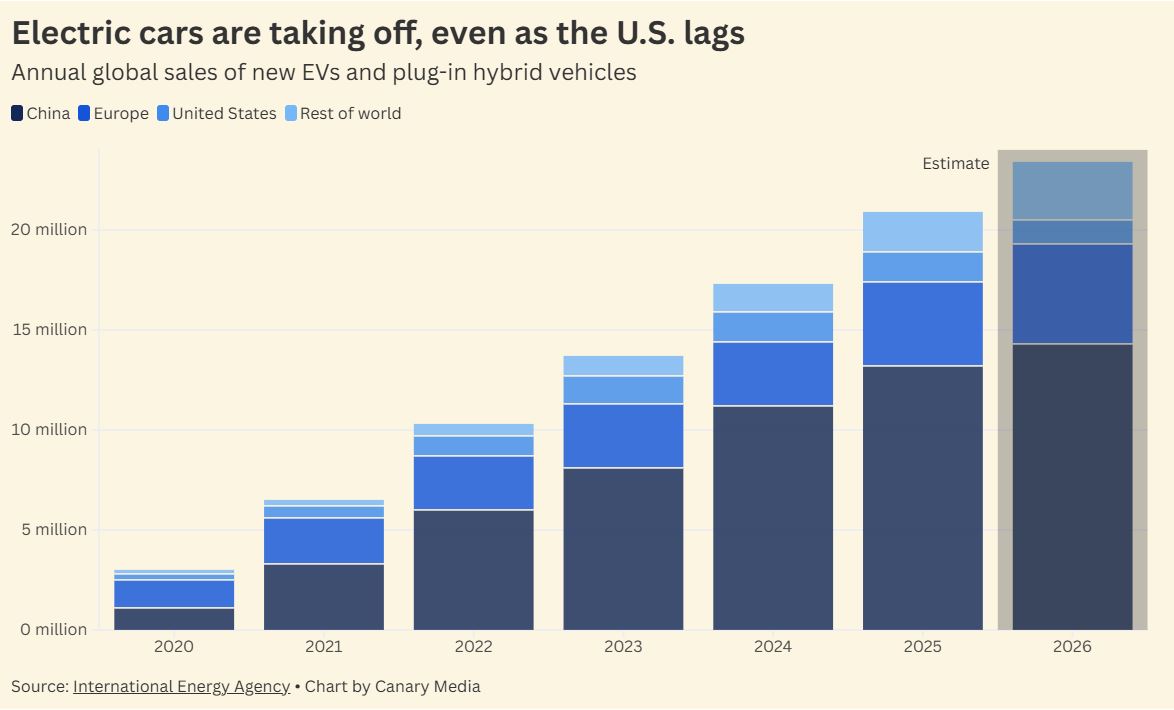

Despite sluggish EV sales in the U.S., it’s full steam ahead for electric vehicles in most other regions.

Electric vehicles may be struggling to find buyers in the U.S. — but they’re making inroads elsewhere.

A record-breaking 28% of new cars sold this year will be battery-powered, according to new data from the International Energy Agency. That’s a big deal: Driving around in gas-guzzling vehicles spews tons of planet-warming and health-harming pollution into the atmosphere.

The latest projections come even as the Trump administration’s attacks on electric vehicles stymie sales in the U.S., the world’s second-largest car market. The country is a massive laggard when it comes to EV adoption, with electric models making up just around 10% of new car sales. New EV sales are expected to decline for the second year in a row in the U.S., though used models are surging in popularity.

But outside the U.S., the picture is very different. The clearest example of that contrast is China, the world’s biggest car market and the global leader in electric vehicle and battery manufacturing. Nearly 60% of cars sold in China this year will be electrified.

EV sales are growing rapidly across the rest of Asia, too. This year, sales are expected to leap by over 50% across Asian countries other than China, IEA found, driven in large part by the availability of super affordable Chinese EV models.

In Europe, which has strong emissions standards that push consumers toward EVs, sales are growing especially fast. This year, EVs will make up one-third of new cars sold in the region, powered not only by EV-adoption poster child Norway but also by rapid uptake in Germany, the U.K., and Turkey.

It’s worth emphasizing that these figures are for new car sales only. It will take longer for EVs to become the most popular type of car on the road: Right now, they make up just about 5% of the global car fleet.

Still, we’re well past the peak for gas car sales, and the trends are in favor of EVs. By 2035, the IEA expects half the new cars sold worldwide to be EVs. In China and the E.U., 90% of new cars could be EVs by that time.

And then there’s the war in Iran, which has caused the price of gasoline to surge and even resulted in fossil-fuel shortages in some countries. The crisis is adding more urgency to the transition to electric vehicles, particularly for nations that rely on imported oil. As EVs get cheaper and the volatility of fossil fuels becomes more apparent, economics may start to drive the transition from gas cars faster than climate goals ever could.

Three electric school buses will kick-start the state’s groundbreaking vehicle-to-grid pilot program once school’s out, with more EVs to be added in the coming months.

After the school year ends in the Massachusetts towns of Acton and Boxborough, the district’s electric buses will mostly stay put in a parking lot. But they won’t sit idle all summer.

The three vehicles will charge up their nearly 200-kilowatt-hour batteries overnight, when the power supply is at its cleanest and cheapest, then send energy back to the grid from 4 p.m. to 7 p.m. on days when the grid is strained. The district will earn revenue for the power it shares, perhaps even enough to cover the costs of charging up during the school year, said Kate Crosby, energy manager for the Acton-Boxborough school district. Plus, the strategy will help lower the emissions and cost of the region’s electricity supply.

“The more we plug in batteries to the grid, the less we use peaker plants,” Crosby said. “They will help to stabilize the grid, help to reduce the cost of electricity for all ratepayers, and they’ll help make the grid cleaner.”

Acton-Boxborough’s school buses are the first vehicles to plug in to a Massachusetts program that aims to demonstrate and investigate the potential of “vehicle-to-everything” technologies, more commonly known as V2X. These systems use bidirectional chargers, which can power up a vehicle as well as send the energy stored in an EV’s battery back to a building or the grid.

Supporters say V2X technologies can yield a host of benefits. They can lower emissions by using stored energy generated at times when the grid is consuming less fossil fuel. They can help users offset their electricity bills by compensating them for power sent to the grid. They contribute to resilience when the power goes out. Plus, they can keep prices lower for everyone by sending cheaper power to the grid during times of high demand.

So far, however, widescale adoption has been elusive. Pilot programs across the U.S. and abroad have tested the possibilities, but they haven’t gained much traction in the face of high upfront costs, technical complexity, the huge variation among what equipment works with what vehicles, and the lack of established plans to compensate users for the power they pour back into the grid.

Massachusetts hopes its initiative will make some headway against these obstacles. At an event last week, the planners behind the demonstration program discussed what they’ve achieved so far, what they’ve learned along the way, and what problems remain.

The Massachusetts Clean Energy Center, an economic development agency, announced the demonstration program in early 2025, with the goal of giving away up to 100 bidirectional chargers to a variety of users. Participants were announced in February 2026: five school districts, four municipalities, and 30 residents. In order to understand how the systems function in a wide range of settings, the planners selected projects in all geographical corners of the state, and in rural, urban, and suburban areas served by 10 different utilities. The installations will include six different types of chargers plugging into eight different vehicles, from buses and pickup trucks to SUVs and compact hatchbacks.

“It’s not just about getting the right vehicle and the right chargers,” said Sally Griffith, transportation electrification program manager for energy consulting firm Resource Innovations, which is working with the state to run the program. “It’s about the whole system — how all of this needs to work together,” she said at the event.

Between 10 and 15 chargers are now installed and awaiting authorization to begin bidirectional charging. The rest are expected to be online by September.

Already, some challenges have been identified. The most pressing, speakers at the event said, have to do with finding a financial model that works.

For one, the systems are pricey: $15,000 to $40,000 for a residential setup, the Massachusetts Clean Energy Center estimates. Pilot programs can help defray costs for small numbers of users for a limited time, but a long-term, reliable compensation plan is needed to get any meaningful number of EV owners to make the leap.

But it turns out those compensation programs can be tricky to design. In Massachusetts, one major discovery so far has been the conflict between state solar incentives and the ConnectedSolutions program, which compensates battery owners for sending power onto the grid. Existing technology can’t tell the difference between electrons sent from solar panels and those coming from batteries. For a home with both solar panels and a bidirectional charger, it would be impossible to separate the solar power that should receive net-metering incentives from the EV battery power that would receive payment from ConnectedSolutions.

The Massachusetts Clean Energy Center had to immediately disqualify roughly 75% of the nearly 300 residential applicants for the V2X program because their homes had solar power, said Elijah Sinclair, the center’s senior program manager.

The state was aware there might be a conflict, but the scale took program planners by surprise, delaying the selection of participants and therefore the deployment of chargers.

One possible answer could lie in a program that compensates virtual power plants — networks of distributed energy resources like solar panels, batteries, and demand management — rather than providing different incentives for each component of the system, Steve Letendre, senior adviser at the Vehicle-Grid Integration Council, an EV charging advocacy group, told event attendees.

“We believe it’s a mechanism by which we can bring EVs onto the grid in a way that maximizes their value,” he said.

An unexpected bright spot so far has been the ease of interconnection, the process of formalizing agreements with utilities for hooking up an energy resource to the grid, Sinclair said.

“Utility interconnection was expected to be a big barrier,” he said. “But everyone has been just awesome to work with, and interconnection hasn’t slowed us down.”

The Massachusetts Clean Energy Center will collect data from participants for the rest of the year. By the end of the year, it aims to publish a comprehensive guidebook on what it’s learned about the cost, system design, and technical and regulatory barriers, with the goal of helping other agencies and states replicate the program.

In the meantime, the students and bus drivers of Acton-Boxborough will be enjoying quieter rides without any diesel fumes, said Crosby, the district energy manager.

“We are improving their quality of life immediately, and helping to create a cleaner, more stable future for them,” she said. “There’s nothing that matters more to us.”

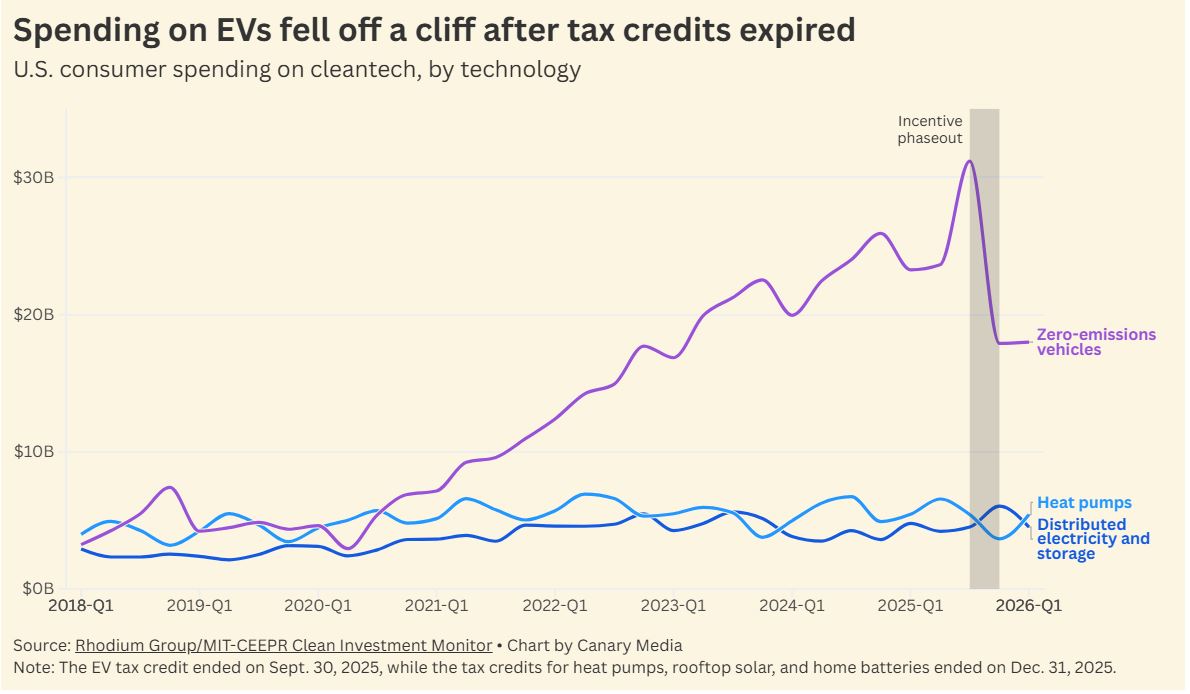

President Donald Trump and the GOP phased out tax credits for all forms of consumer cleantech last year — but EVs took the biggest blow.

Once upon a time, Americans could get big federal tax incentives for buying electric vehicles, heat pumps, rooftop solar, and home batteries. But the Trump administration scrapped those tax breaks last year — and no category of household cleantech has suffered more as a result than EVs.

Consumer spending on EVs has fallen off a cliff since the phaseout of the $7,500 federal tax credit at the end of last September.

In a rush to snap up that incentive before it disappeared, Americans spent a record $31 billion on EVs in Q3 2025 — only for that figure to plummet to around $18 billion for each of the last two quarters, per new data from the Clean Investment Monitor, a joint project of Rhodium Group and the Massachusetts Institute of Technology’s Center for Energy and Environmental Policy Research.

It’s the equivalent of turning back the clock to early 2023 in terms of spending on EVs, which made up nearly 10% of new car sales in the U.S. in 2025.

The effects have been less dire for other consumer cleantech, like distributed electricity and storage — primarily rooftop solar and home batteries — as well as heat pumps.

Under the 2023 Inflation Reduction Act, consumers could access tax credits that covered 30% of the cost of rooftop solar and home storage systems with no cap, as well as incentives that covered 30% of heat pumps up to a limit of $2,000 per tax year. The One Big Beautiful Bill Act eliminated those incentives last December.

Investment in rooftop solar and home batteries didn’t drop as dramatically after the expiration of the tax credits, and sales of heat pumps actually rose a little in Q1 2026.

That suggests the EV tax credit was more motivating to Americans than the other incentives.

But the decline in EV sales so far this year may also be explained in part by broader trends in the auto sector. In the U.S., overall new vehicle sales were down nearly 7% year over year in Q1. In the current volatile economic climate, people are just buying fewer new cars.

Regardless, the bottom line is clear: New EVs are selling slowly in the U.S., far slower than in many other parts of the world, and far slower than climate advocates had hoped for. It’s unclear when the market will recover from its post-tax-credit malaise, but in the meantime, there is a bright spot: Used EVs are about the same price as used gasoline cars, they’re increasingly available, and they’re flying off lots.

A developer building chargers at home-improvement stores discusses the promise — and pitfalls — of siting EV infrastructure in major retailers’ parking lots.

Menards is a Midwest staple: The Wisconsin-based chain, known for its “Save BIG Money” slogan, is the nation’s third-largest home-improvement retail brand, behind Home Depot and Lowe’s. But in Illinois, it’s slowly becoming more than just a place for folks to pick up ceiling hooks and gardening gloves, as developers eye the big-box store as a promising spot to build public EV chargers.

Two companies — JOJO Superfast EV Charging and charger manufacturer XCharge North America — announced last month that they aim to install chargers across nine of the brand’s Illinois stores. They’ve already outfitted two suburban Chicago Menards with four dual-port chargers, meaning eight cars can charge simultaneously at each store, and another suburban Chicago site is under construction. These add to the chargers that other firms have already installed at Menards in other cities, including the Chicago suburb of Dolton.

While these projects may be limited in scale, they represent a key strategy to convince more people to get EVs: make it convenient to charge as they go about daily routines.

“People in the Chicagoland area really enjoy going to Menards,” said Alex Urist, co-founder and senior vice president of marketing at XCharge North America, noting that as a Northeasterner, he was intrigued by the Midwestern affection for the company.

Installations like these “have a direct effect on the adoption of EVs, because they increase the perceived — and actual — availability of chargers” in places people visit regularly, he continued.

The U.S. currently has tens of thousands of public chargers and counting, located along highways as well as at parking garages, shopping centers, hotels, and public buildings. But that growth will need to continue to get more consumers comfortable with electrifying their ride. This is especially true in states with ambitious electrification goals like Illinois, which aims to get 1 million EVs on the road by 2030. Meeting such targets became more challenging last year as the Trump administration axed federal EV incentives and tried to freeze billions in funding for charging networks, although Iran war–driven gasoline price spikes and increasingly cheap used EVs may bolster the market.

Big-box stores anchored in suburban shopping centers are natural places for EV chargers. People frequently drop by to run multiple errands and grab lunch or coffee, so they can charge as they check items off their to-do list.

“At the end of the day, this business is about real estate,” Urist said. “The charger works when it’s in the right place.”

Urist feels that big-box stores are among the “different pockets emerging” as EV charging sites. “Walmart is really leading the charge on this,” he said, and Ikea has ports at nearly all its U.S. locations.

But installing chargers at big-box stores and outdoor malls involves overcoming some hurdles. For one thing, the company that owns the store may not own the parking area. And identifying the right location for chargers within sprawling lots is not easy: Ideally, the chargers would be near a store’s entrance for convenience’s sake, but that might be far from the hookup to the local grid, creating extra costs and construction.

“Adding 25 feet can add an additional $10,000 in conduit work and trenching,” Urist said.

Putting chargers behind a store, if that’s where the nearest power source is, runs the risk that drivers don’t realize the ports are there, and may make it less convenient for shoppers to walk to nearby establishments. Meanwhile, charger installation and maintenance may threaten to block off parts of a parking lot or store access for periods of time.

“EV charging and infrastructure development is a lot more challenging than customers see,” Urist said. “People say it would be great to have chargers at McDonald’s. I’ve looked at a few McDonald’s. It gets logistically difficult. Is the location going to impact how that drive-through functions? Are you going to have clogs in the parking spaces?”

The number of partners who must collaborate to make such projects a reality adds to the complexity.

For the Menards project, XCharge North America supplies the chargers, monitors them, and offers an extended warranty that includes labor and parts. JOJO Superfast, which owns and operates the chargers, collects revenue from drivers who use them.

ComEd, the utility serving northern Illinois, is considering funding the site preparation for the two Menards stores with operational chargers through its “make-ready” rebate program. The state of Illinois is also providing incentives through its clean energy programs, according to Kim Biggs, spokesperson for the Illinois Environmental Protection Agency. State legislators helped make it all possible by passing laws with ambitious clean energy mandates and funding. Over the last three years, he state has funded chargers at over 575 locations, almost a third of which are up and running, according to a state map.

“As the federal supports dissipate, states and utilities are increasingly required to assume a greater role in driving continued EV market growth and ensuring the timely deployment of essential charging infrastructure,” Biggs said.

She called the Menards project “a strong example of how public funding and private-sector collaboration can accelerate deployment of EV infrastructure in practical, high-use settings.”

Urist said that one of XCharge’s products could be particularly useful at big-box stores and similar locations. The company’s GridLink is essentially an EV charger outfitted with a small battery that can fill up on grid power or from an on-site solar panel.

“It can pull power from the grid slowly throughout the day and store it so that when an EV pulls up, the charger pulls from both the grid and its internal battery simultaneously,” Urist explained, noting that over 25 GridLink units have been deployed across the U.S. and Canada.

The battery can reduce strain on the grid, allowing GridLink to be installed in places with less built-out electrical networks. “It’s a great way to get high-speed [charging] infrastructure into communities that have traditionally been overlooked in the energy transition,” Urist said.

For example, a GridLink unit is helping Detroit electrify its municipal fleet, providing charging at a Department of Public Works site with a limited grid connection, he said.

Urist noted that GridLink chargers could also provide vehicle-to-grid services, wherein a utility pays a charger owner for providing storage on the grid.

ComEd does not currently offer a vehicle-to-grid program but is studying the possibility, and it launched a pilot last year involving school buses.

“Even when a project does not directly provide grid services today,” ComEd spokesperson Anthony Garcia said, “installations like this help inform how ComEd designs infrastructure upgrades, demand management strategies, and future programs that ensure EV charging can grow without compromising reliability for all customers.”

With gas prices up and more affordable options hitting lots, used EVs are looking like a sweet deal. We offer some useful tips to help you make the best purchase.

A year ago, Crystal Bright was freaking out. The Charlotte, North Carolina–based interior designer had just separated from her partner and needed to figure out how to stay afloat financially.

She could have taken on more work, Bright said, but that would have meant spending less time with her son, who’s now 8 years old. So she reasoned, “Let me just save money instead of figure out how to make money.”

A used electric vehicle turned out to be the key to solving her financial woes.

Last May, she bought a 2013 Nissan Leaf for $3,000 outright. That let her cut her $400 monthly payment on her previous car and liberated her from the $200 a month she used to pay for gas. The lower maintenance cost of owning an EV has also put another $200 back in her pocket each month. With $800 total per month in savings, Bright has been able to move with her son from an apartment in which she didn’t feel safe to a “beautiful townhouse.”

Across the U.S., gasoline prices have spiked to $4.50 per gallon on average because of the war in the Middle East. But Bright is able to recharge mostly using the copious free public charging available locally, and she can top off at home with her 100-foot extension cord if she needs to. “I have no idea what gas costs, thank goodness,” she said.

More drivers want to be insulated like that. The market for used EVs is surging; their average cost of $35,895 is now competitive with that of used gas cars (average $34,799).

If you’re interested in buying a used EV for the financial savings — not to mention reduced air and climate pollution — here’s how to make sure you get one that’s right for you.

Figure out what range you actually need, based on how much you typically drive and how frequently you’ll charge, recommends Desiree Moore, program manager at Drive Clean Colorado, a state program that aims to reduce greenhouse gas pollution from vehicles.

On average, Americans are on the road less than 30 miles a day. But Moore often drives long distances for work, so she’s eyeing a newer Leaf or Ford Mach-E to get at least 200 miles to 300 miles on a single charge, she said. InsideEVs, U.S. News & World Report, and Recurrent, a company that aggregates data on vehicle battery health, are a few of the sources that list their top used EV picks, which will give you a sense of the best range for your buck.

Also get familiar with the discounts available in your area. While the Trump administration vaporized federal tax credits for new and used EVs, nonprofits Veloz and Rewiring America have tools to help you look up local incentives.

But the most important EV research might be what you do in person. “Drive as many as you possibly can, because there’s such a difference in driving style and acceleration and turning radius — all of the things that you would expect from any used car,” said Andrew Garberson, Recurrent’s head of growth and research.

Potentially hundreds of dollars a year or more, depending on several factors, including your current car, how much you drive, shifting gas prices, and whether you can charge on the cheap, like at home with a discounted EV rate from your utility — or, less commonly, for free like Bright does. Filling up at home in 2026 can be like buying gas at $1.60 per gallon.

You can play around with different online tools to get a sense of the savings that come with switching to an EV. For example, the U.S. Department of Energy’s Vehicle Cost Calculator lets you compare the total cost of ownership for specific vehicle makes and models. And while the AFLEET TCO Calculator from DOE’s Argonne National Laboratory doesn’t have that capability, it allows you to toggle the cost of electricity. (The Vehicle Cost Calculator auto-sets power prices based on your state, though you may be able to get a better rate with your utility.) Both tools let you input the current price of gas.

Here’s an example from giving the AFLEET tool a spin: Under the assumptions of driving 12,400 miles per year, $3.50-per-gallon gas, and Xcel Energy Colorado’s best time-of-use rate of about $0.08 per kilowatt-hour, the calculator estimated that over 10 years an EV would save more than $11,000 in fuel costs and more than $8,000 in maintenance.

Beyond running an Internet search for “used EVs near me,” look to local dealers, many of which have upped their EV game. Bright scoped out listings on Carvana, and ultimately went with a car she found on Facebook.

You can also check out online marketplaces such as Edmunds and Cars.com. These platforms include Recurrent’s forecasts on vehicles’ remaining range, which are based on real-world driving data shared by more than 30,000 vehicle owners.

The heart of an EV is its battery. Info on its condition might be available in an online listing, as mentioned above.

But you can do a live check, too. When you turn the EV on, take a look at its current charge and estimated range and compare that with the predicted range on a full charge, Recurrent’s Garberson said. As you take it for a test drive, make sure the figures on the dash don’t nosedive.

Battery replacements, while rare, typically cost $5,000 to $16,000. So it’s worth taking the time to ask the dealer for relevant information. Drive Clean Colorado has a handy checklist of questions: “Has the battery ever been serviced or replaced?” “What’s the remaining battery warranty?” “Is the warranty transferable to a second owner?”

Be sure to ask for a copy of the battery’s health report, which includes a “State of Health” metric that clarifies loss of capacity. For example, a score of 95% means that if the original range was 300 miles, it’s now 285 miles.

Warranties usually cover the battery and drive train for at least eight years or 100,000 miles. Verify in the contract what’s covered for the car you’re eyeing.

Vehicles that are 2 years to 4 years old are an especially good bet, according to Ingrid Malmgren, senior policy director at EV advocacy nonprofit Plug In America. “Those are the vehicles that are going to be coming off of leases. They tend to be lower mileage [and] have lots of remaining life left in them.”

EVs can last 150,000 miles to more than 300,000 miles; and the batteries, losing on average about 2% of their original mileage annually, have a typical lifespan of about 13 years. And the technology keeps improving.

“Mileage has less of an impact than battery health on longevity,” Malmgren said. “So if you wouldn’t buy a gas car with 100,000 miles, an EV with good battery health still could have hundreds of thousands of miles left, because [it has] fewer moving parts.”

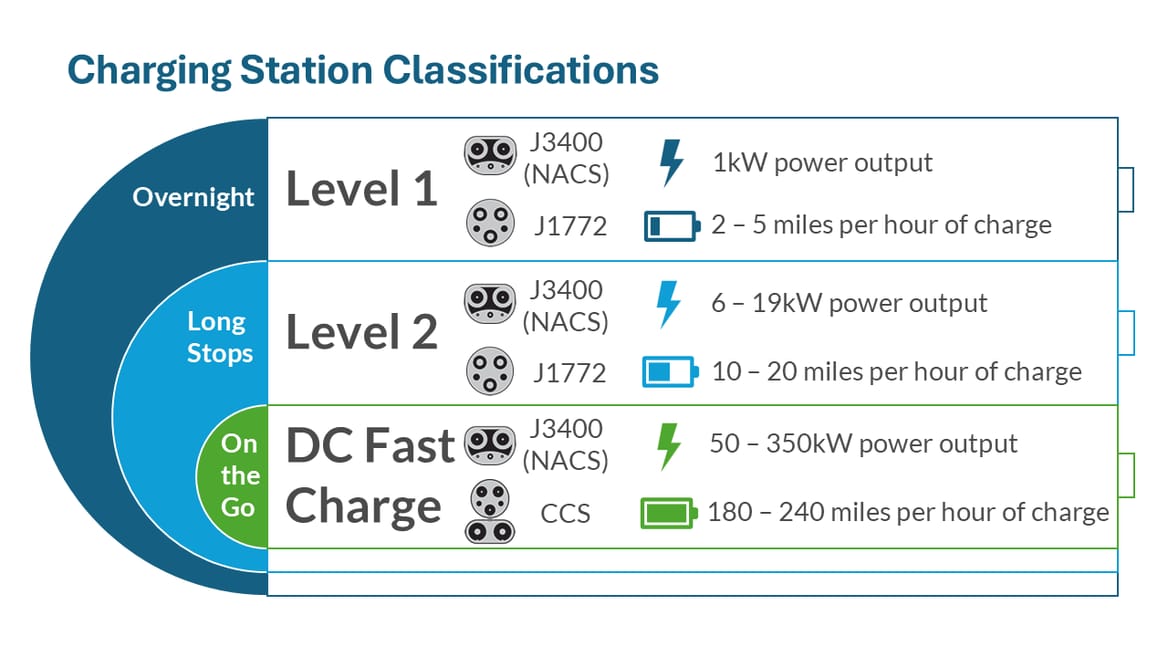

Check the EV charging port. Older vehicles might have a J1772 port, which is compatible only with Level 1 and Level 2 chargers, instead of a CCS or NACS port that can accommodate direct-current fast-charging, too. DC fast charging can be 10 times as quick as Level 2 charging.

If you’re planning to plug in at home, you might want to install a Level 2 charger before you drive the car off the lot. Some of the best-reviewed options retail for about $200 to $900. A 120-volt outlet will provide a trickle of about 2 miles to 5 miles of charge per hour, depending on the vehicle.

Each EV make and model will also have its own max charging speed, which could influence how you road-trip. An old Chevy Bolt that taps out at 50 kilowatts will take more than an hour to fully recharge even at the fastest charger, whereas the newer model could do that in less than 20 minutes.

Bright, whose Leaf gets a max of about 68 miles of range, would love to go farther. So now she’s saving up for her next EV: a 2025 Nissan Leaf with 149 miles on a full charge. Bright plans to shop used because it’s so much more affordable; she has seen prices for secondhand models around $18,000, deeply discounted from the roughly $30,000 sticker price of a new one.

Bright’s bank account steadily grew after she switched to a used EV. “I felt so much relief,” she said. “I recommend it for anybody [who’s] struggling.”

European drivers are escaping high gas prices and buying more cheap Chinese EVs. In the U.S., that’s impossible.

This analysis and news roundup come from the Canary Media Weekly newsletter. Sign up to get it every Friday.

As the war in Iran spikes gasoline prices around the globe, drivers in many countries have headed for an obvious emergency exit: EVs. But buyers in the U.S. aren’t following suit, and a lack of affordable EV options is a big reason why.

While global EV sales plunged in January and February from 2025’s record heights, they rebounded in March and April, according to data out this week from Benchmark Mineral Intelligence. That’s largely thanks to a surge in Europe, where EV sales were 27% higher this April than the same month last year. Rising gasoline prices fueled the region’s market, BMI says, as did the increasing availability of cheap Chinese EV imports.

The latter is exactly what the U.S. lacks. While used EVs are now cost-competitive with used gas cars, that’s not the case for new models. The cheapest new EV sold in the U.S., the Nissan Leaf, starts at just under $30,000. But in China, dozens of EVs retail for around $25,000 or less, including several models from BYD, which surpassed Tesla as the world’s top EV seller earlier this year. And while the Asian superpower has ramped up exports to Europe, Latin America, and, more recently, Canada, its cars face a 100% tariff and national security rules in the U.S. that make them impossible to sell.

It’s not that U.S. drivers aren’t interested in electrifying their ride. Shopping sites Cars.com and CarGurus both say searches for EVs have jumped since the Iran war began. And a February survey from Cox Automotive found nearly half of Americans considering an EV would pick the Chinese-made Geely Xingyuan over a Tesla Model Y, while 38% would select BYD’s Seagull over the Tesla.

But letting Chinese EVs into the U.S. is a scary prospect for domestic automakers. The American EV sector is only just finding its sea legs, having been knocked back time and time again by tariffs, politics, and the federal tax credit rollback. It’s probably not reassuring that President Donald Trump has said he’s open to Chinese investment in the U.S., provided companies use American labor — and that Trump’s meetings this week with Chinese President Xi Jinping similarly indicated a softening in relations.

“[U.S. automakers are] absolutely more than worried — they’re scared stiff,” Michael Dunne, chief executive officer of automotive consultancy Dunne Insights, told Politico. “Imagine if the Chinese come in with a $25,000 EV. That could catch like wildfire.”

For now, though, BYD in the USA remains miles down the road — if it’s a destination we ever reach at all.

On wind and solar, Interior won’t go down without a fight

Interior Secretary Doug Burgum on Wednesday affirmed that the Trump administration will appeal a ruling that struck down Interior Department policies stymieing wind and solar permitting.

Last month, a federal judge ordered the administration to stop enforcing five actions that effectively blocked all wind and solar energy permitting on public land, including a policy that required Burgum to personally sign off on projects that need federal permissions. The blockade was “arbitrary and capricious,” the judge said, especially considering permitting for fossil fuel companies marched on as usual.

Congress has been trying for years to enact bipartisan legislation to reform energy permitting, but Trump’s anti-renewables crusade has led Democrats to repeatedly back out. This appeal is likely to derail reform attempts once again, as two senators said last month they’d cooperate only if the Interior Department lets solar and wind projects keep rolling.

Geothermal innovation keeps heating up

This week marked a milestone for the geothermal industry — a potentially key piece of the push to secure clean, 24/7 power.

On Wednesday, Fervo Energy became the first next-generation geothermal company to go public, bringing in $1.9 billion from its IPO and securing a valuation of about $7.7 billion, Canary Media’s Dan McCarthy reports. While traditional geothermal energy production has been limited to certain geologic areas, like volcanic regions, Fervo is borrowing drilling techniques from the fossil fuel industry to access deep-down heat in more locations.

Another thing geothermal may be able to borrow from oil and gas drillers? Their abandoned wells. The U.S. is littered with these sites, many of which have no clear owner and are polluting the air and groundwater, Canary’s Maria Gallucci reports. A growing number of both Republican- and Democratic-led states are exploring whether these wells could be repurposed for geothermal energy production — a complicated task with huge potential upside.

Fossil fuels all the way down: In rural Jasper County, Indiana, residents are fighting to shut down a 50-year-old coal plant running past its prime, while also staring down another polluting prospect: a new gas plant to power a data center. (Canary Media)

Tapping the brakes: President Donald Trump says he supports suspending the federal gas tax, though even Republicans in Congress are reluctant to move on his call to action. (Politico)

Clean power climbs: A new dashboard that tracks national and state-level progress on deploying clean energy finds that the U.S. produced nearly three times as much solar, wind, and geothermal power in 2025 as it did in 2016. (Environment America, news release)

Generating controversy: Elon Musk–led company xAI has installed dozens of “temporary-mobile” gas turbines in Mississippi to power its data centers, which remain exempt from state oversight even as neighboring residents push back over pollution and noise concerns. (Mississippi Today)

Inside offshore wind communities: After months spent interviewing residents in three offshore wind hubs in Connecticut, Maryland, and Massachusetts, researchers find that communities are excited by the projects’ economic promise but are unsure it’ll last once construction is finished. (NBC Connecticut)

Georgia’s nuclear warning: Utility customers are still paying the cost of Georgia Power’s addition of nuclear reactors to Plant Vogtle, which ran seven years behind schedule and more than two and a half times over budget, providing a cautionary tale for advocates of the energy source. (Inside Climate News)

Mercury rising: Coal power plants released 9% more mercury in 2025 than they did a year earlier — a number that will likely grow as the Trump administration looks to expand coal power generation and loosen regulations that could curb the toxic pollutant. (New York Times)

.svg)